Signing a new contract is a very exciting milestone. You have worked hard to get this far and are likely thrilled to be progressing in your rugby career. Plus, you may now be earning more than you ever have before.

While earning a much higher salary is a positive step, it means you may need to pay closer attention to tax. If your new contract comes with a pay increase that pushes you into a higher Income Tax bracket, more of your money will be eroded by tax than before.

This is especially important if you are set to earn more than £100,000 a year.

Continue reading to discover how Income Tax brackets work, what you can do to lessen their impact, and how we can help.

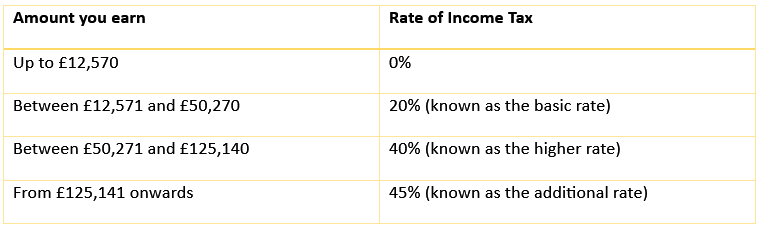

How UK Income Tax brackets work

Taxpayer earnings fall into “brackets” for the purposes of calculating Income Tax. The more you earn, the higher rate of tax you are likely to pay.

Frozen at their existing rates until 2028, the UK Income Tax brackets are shown in the table below.

On top of this, you will pay National Insurance contributions (NICs) to the government.

So, if you previously earned £90,000 a year:

- You would likely have paid £23,432 in Income Tax, excluding NICs and any deductions such as pension contributions, which we will come to later.

- Your take-home pay would have been approximately £62,757 after Income Tax and NICs.

If you now earn £130,000 a year:

- Your Income Tax bill will rise to £44,703 excluding NICs and deductions.

- Your take-home pay will be approximately £80,686 after Income Tax and NICs.

Some earnings above £100,000 create a 60% Income Tax trap

As you can see in the example above, although your salary would have risen by £40,000, your take-home pay would only go up by around £18,000.

This is partly because of the 60% Income Tax trap.

Once your earnings exceed the £100,000 threshold, you begin to lose your tax-free Personal Allowance of £12,570. For every £2 you earn over £100,000, you lose £1 of your Personal Allowance, meaning it disappears completely at £125,140.

This creates an effective Income Tax rate of 60% for earnings between £100,000 and £125,140.

Essentially, if your salary went up to £130,000, instead of paying Income Tax on some of your earnings you would pay it on all of them. Plus, some of your earnings would be taxed at an effective rate of 60%.

If you earn over £100,000 a year, you may lose access to free childcare

If you have children, it is worth noting that you lose some childcare benefits, subsidised by the government, once you start earning £100,000 or more.

This is a hard stop. Parents who earn less than £100,000 a year can claim up to 30 hours of free childcare for 38 weeks of the year, depending on how old their child is and several other factors. This is known as Free Childcare for Working Parents. There is also Tax-Free Childcare, an additional subsidy available from the government, providing up to £2,000 a year.

But if you or your partner earns an “adjusted net income” (more on this later) of £100,000 or more, you are not eligible for any of the above schemes. This means nursery and childminder costs will be entirely funded by you.

Strategic pension contributions could help you bring your Income Tax bill down and retain childcare benefits

If you receive a salary bump after signing a new contract and enter a new tax bracket or start earning more than £100,000 for the first time, a large portion of your earnings may not make their way into your pocket.

That is, unless you make strategic pension contributions to bring your adjusted net income down to keep more for yourself and your loved ones.

Here is how it works in two steps.

- Pay a portion of your salary into your pension

As an athlete, you will already know that you may retire earlier than most and need a foundation of wealth to draw from when you are older.

Using the earlier example of receiving a pay increase to £130,000 a year, you could decide to put £31,000 a year into your pension, to reduce your income to £99,000.

While you will not be able to access this money until the Normal Minimum Pension Age (NMPA) of 55, rising to 57 by 2028, there are several good reasons to take this approach.

Firstly, that phrase you read earlier, “adjusted net income”, is your income minus tax-deductible payments like pension contributions.

So, if you brought your salary down to £99,000 a year, you would:

- Pay less Income Tax

- Retain some free childcare benefits

- Increase the size of your pension pot.

Not only would you reduce your Income Tax bill, but you would also be helping your future self to achieve greater financial comfort.

- Claim tax relief and save more for your future

For most earners, and as of the 2025/26 tax year, there is a pensions Annual Allowance of £60,000. This allowance covers all contributions combined, including those made by an employer, for the tax year. Up to this threshold, you can make tax-efficient pension contributions. If eligible, unused Annual Allowance from the previous three tax years can also be used to increase the overall figure.

In addition, as long as your own contributions don’t exceed 100% of your earnings, you will receive tax relief on what you put in.

You will benefit from 20% tax relief from the government upfront so you only pay in 80% of the contribution. If you are a higher- or additional-rate taxpayer, you can claim additional tax relief up to your marginal rate of Income Tax by completing a self-assessment tax return each year or contacting HMRC (higher-rate only). Your accountant and financial planner will be able to help you with this.

Tax relief makes your pension contributions even more valuable, giving your wealth the best chance to grow within your pension and provide a foundation to draw from later in life.

A financial planner can help you secure a bright future

If you are taking big steps in your career and need specialised advice, we are here for you.

Our team of financial planners works with athletes on tax mitigation, future planning, and protecting earnings against the unexpected.

Email enquiries@dbl-am.com or call 01625 529 499 to speak to us today.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

All information is correct at the time of writing and is subject to change in the future.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate tax planning.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

Workplace pensions are regulated by The Pensions Regulator.