Property could be a useful investment for rugby players for two reasons. First, as house prices continue rising, you may see significant appreciation in the value of your investment. Additionally, you could earn a regular income from a rental property.

Having this alternative income source may be particularly beneficial when you finish playing and transition to a new career.

However, there are certain tax implications to consider with investment properties, and if you do not plan accordingly, a large bill could reduce your returns.

Read on to learn about three taxes you may pay when investing in property.

1. Stamp Duty Land Tax

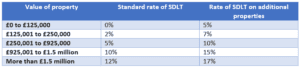

Normally, when you purchase a property, you must pay Stamp Duty Land Tax (SDLT), and the amount depends on the value of the property.

There are several brackets of SDLT, so you pay a higher percentage of tax on certain portions of a property. Additionally, if you are purchasing a second property, the rates of SDLT are higher.

The following table shows what you could pay.

You pay the different rates of SDLT on each portion of the value of a property.

For example, if you purchased a buy-to-let property for £300,000, you would pay:

- 5% on the first £125,000 (£6,250)

- 7% on the value between £125,001 and £250,000 (£8,750)

- 10% on the value between £250,001 and £300,000 (£5,000).

This leaves you with a total SDLT bill of £20,000.

It is important that you factor this cost in when deciding whether to purchase a property because SDLT can significantly increase your initial outlay. This means that you need to see more growth in the value of the property before you can recoup your investment.

2. Income Tax

If you rent out a property, you may pay Income Tax at your marginal rate on any funds you receive.

This is calculated in the same way as Income Tax on your salary. The first £12,570 is tax-free, and you then pay varying rates of tax on different portions of your income.

Each year, you have a £1,000 tax-free Property Allowance you can use. Alternatively, you can deduct certain expenses such as maintenance costs, utility bills, professional fees, and admin costs.

You must choose either the Property Allowance or add up your total expenses, not both. Typically, if your allowable expenses are less than £1,000, you will choose the Property Allowance. Otherwise, you can deduct all available costs.

After making the necessary deductions, you will then pay Income Tax at your marginal rate on the remaining rental income.

For example, if you earn £60,000 from playing and another £10,000 from rental properties, you would be a higher-rate taxpayer.

If you decide to use your £1,000 Property Allowance, you would then pay 40% Income Tax on the remaining £9,000.

This leaves you with a bill of £3,600.

However, the government recently announced that the Income Tax rates for landlords would each increase by two percentage points from 6 April 2027.

Using the above example, this means you would pay £3,780 once these changes come into effect.

As such, property investors could lose more of their income to tax in the future, making profit margins smaller.

3. Capital Gains Tax

When you purchase a property, it will hopefully appreciate in value, meaning you can later sell it for a profit.

This might be a useful way to unlock wealth in later life to help you fund your lifestyle as you transition to a second career, start a business, or even fund your second retirement.

However, when selling a property that is not your main home, you may pay Capital Gains Tax (CGT) on the profits you earn.

As of 2026/27, the first £3,000 is free from CGT; this is your Annual Exempt Amount. You then pay a different rate depending on which Income Tax bracket the gain falls into.

For example, if you purchased an additional property for £250,000 and later sold it for £300,000, you would make a profit of £50,000.

Provided these were your only gains in the year, you would apply the Annual Exempt Amount, meaning you pay CGT on the remaining £47,000.

If the entire gain fell within the basic-rate bracket, you would pay £8,460 in CGT.

However, if you are earning income from elsewhere, the entire gain might fall into the higher- or additional-rate bracket. This would mean you pay £11,280.

If capital gains push you from the basic-rate into the higher-rate bracket, you will pay CGT at 18% on part of the gain and 24% on the rest.

A large CGT bill could reduce the amount of wealth you receive when selling an investment property, potentially disrupting certain financial aims in later life.

A financial planner can help you navigate the complex tax landscape

As you can see, the UK tax landscape is complicated and there are several different taxes you might pay when investing in property.

That is why it may be beneficial to work with a financial planner. We can help you understand the tax implications of investing in property and take steps to reduce the amount you pay.

This means you retain more of your wealth to put towards important life ambitions.

Get in touch

If you need guidance about investing for the future and managing your tax liability, please do get in touch with DBL Asset Management.

Email enquiries@dbl-am.com or call 01625 529 499 to speak to us today.

Please note

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate tax planning or buy-to-let (pure) and commercial mortgages.